Automotive Heat Exchanger Market Size & Share 2026-2035

Market Size - By Vehicle (Passenger Vehicles, Commercial Vehicles, Off-Highway Vehicles); By Product (Radiators, Intercoolers, Oil Coolers, Exhaust Gas Recirculation (EGR), Others); By Material (Aluminum, Copper, Others); By Design (Plate Bar, Tube Fin, Others); By Sales Channel (OEM, Aftermarket); By Propulsion (ICE, Electric, Hybrid), Growth Forecast. The market forecasts are provided in terms of value (USD) & shipment (Units).

Report ID: GMI13189

|

Published Date: April 2026

|

Report Format: PDF

Download Free PDF

Authors: Preeti Wadhwani, Aishvarya Ambekar

Automotive Heat Exchanger Market Size

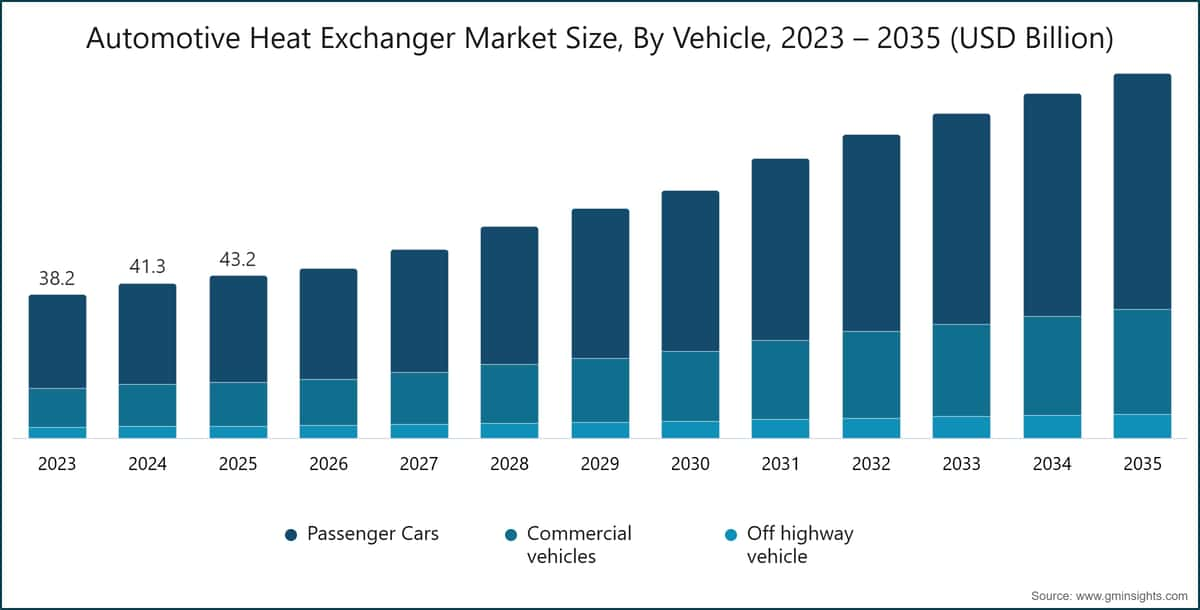

The global automotive heat exchanger market was estimated at USD 43.2 billion in 2025. The market is expected to grow from USD 45.3 billion in 2026 to USD 97.2 billion in 2035, at a CAGR of 8.9%, according to latest report published by Global Market Insights Inc.

Automotive Heat Exchanger Market Key Takeaways

Market Size & Growth

Regional Dominance

Key Market Drivers

Challenges

Opportunity

Key Players

The market volume was estimated at 298.3 million units in 2025. The market is projected to grow from 320.4 million units in 2026 to 497.4 million units by 2035, registering strong double-digit growth over the forecast period.

The rapid evolution of the automotive industry driven by electrification, stricter emission standards, and the need for improved vehicle efficiency is significantly transforming the automotive heat exchanger market. Traditionally limited to engine cooling and basic HVAC applications in internal combustion engine (ICE) vehicles, heat exchangers are now becoming central to managing complex thermal loads across modern vehicles. In electric and hybrid vehicles, they play a critical role in regulating battery temperature, cooling power electronics, and maintaining optimal cabin conditions, thereby directly influencing vehicle performance, safety, and driving range.

Increasing consumer demand for enhanced comfort and premium in-vehicle experiences is further strengthening the importance of advanced thermal systems. Features such as automatic climate control, seat heating and cooling, and multi-zone HVAC systems are driving the integration of highly efficient and compact heat exchangers. At the same time, manufacturers are focusing on lightweight and high-performance materials such as aluminum and composite structures to improve heat transfer efficiency while reducing overall vehicle weight.

For instance, in March 2025, Valeo announced the expansion of its high-efficiency heat pump and thermal system production in Europe to support EV manufacturers in meeting stringent emission norms and improving vehicle range and cabin comfort.

The growing penetration of electric vehicles, along with tightening global emission and fuel efficiency regulations, is accelerating the demand for next-generation heat exchanger solutions. Automotive manufacturers are shifting toward integrated thermal architectures that combine multiple heat exchange functions into a single system. This approach enhances energy efficiency, reduces system complexity, and supports better thermal management across batteries, motors, and electronic components.

Innovation in materials and design is reshaping the competitive landscape of the market. Advanced technologies such as microchannel heat exchangers, compact brazed aluminum units, high-efficiency condensers and evaporators are gaining widespread adoption. In addition, the development of environmentally sustainable refrigerants with lower global warming potential (GWP) is becoming a priority due to evolving regulatory requirements. Companies are also investing in intelligent thermal management systems that leverage sensors and control algorithms to optimize temperature regulation in real time.

Electrification is also influencing heat exchanger requirements across different vehicle segments. Passenger electric vehicles increasingly rely on energy-efficient HVAC systems, including heat pump-based solutions, to enhance driving range under varying climatic conditions. In commercial vehicles and electric buses, heat exchangers are designed to handle higher thermal loads associated with large battery capacities and extended operational cycles. Furthermore, the shift toward high-voltage platforms and fast-charging infrastructure is increasing the need for advanced cooling technologies capable of maintaining thermal stability under high stress conditions.

Digital integration is emerging as a key trend in the automotive heat exchanger market. Modern thermal systems are increasingly connected with vehicle-wide control architectures, including battery management systems (BMS) and electronic control units (ECUs). Advanced software-driven thermal management enables predictive temperature control, pre-conditioning functions, and optimized energy distribution, enhancing both vehicle efficiency and safety. Compliance with global safety standards is also gaining importance, as effective thermal management is critical to preventing system failures and ensuring safe vehicle operation.

North America and Europe represent high-value markets for automotive heat exchangers, driven by stringent emission regulations, fuel efficiency standards, and advanced vehicle technologies. Strong OEM presence and electrification trends increase demand for compact, high-performance thermal systems. Focus on engine downsizing, cabin comfort, and battery efficiency further supports adoption of advanced heat exchanger solutions across passenger and commercial vehicles.

Asia-Pacific is the fastest-growing automotive heat exchanger market due to high vehicle production, rising electrification, and stricter emission norms. China leads demand with large-scale manufacturing, while India, Japan, and South Korea invest in cost-efficient and advanced thermal technologies. Growth in electric vehicles, two-wheelers, and commercial fleets is driving scalable, durable, and energy-efficient heat exchanger adoption across the region.

Automotive Heat Exchanger Market Trends

Automakers are increasingly adopting integrated thermal management systems that combine multiple functions such as engine cooling, battery thermal regulation, and cabin HVAC into a single architecture. This trend reduces component redundancy, improves overall system efficiency, and optimizes energy usage. It is particularly important in electric vehicles, where coordinated thermal control directly impacts battery performance, driving range, and passenger comfort.

For instance, in May 2025, Mahle GmbH introduced an integrated thermal management module combining battery cooling, power electronics, and HVAC functions into a single compact unit, aimed at improving EV efficiency, reducing system complexity, and enhancing overall vehicle energy management.

Microchannel heat exchangers are becoming widely adopted due to their superior heat transfer capabilities and compact design. These systems use smaller channels to increase surface area, enabling efficient heat dissipation with reduced material usage. Their lightweight structure supports vehicle weight reduction goals while maintaining high thermal performance, making them highly suitable for modern vehicles with space constraints and efficiency requirements.

The shift toward lightweight vehicles is driving the adoption of advanced materials such as aluminum alloys, composites, and corrosion-resistant coatings in heat exchangers. These materials improve thermal conductivity, durability, and resistance to harsh operating conditions. By reducing overall system weight while maintaining performance, they contribute significantly to improved fuel efficiency in ICE vehicles and extended range in electric vehicles.

With the rapid growth of electric vehicles, there is increasing demand for specialized heat exchangers tailored for battery cooling, power electronics, and electric drivetrains. These solutions are designed to manage high thermal loads and maintain optimal operating temperatures. Effective thermal management enhances battery lifespan, improves charging efficiency, and ensures safety, making EV-specific heat exchangers a critical area of innovation.

Heat exchangers are increasingly being integrated with sensors and advanced control software, enabling intelligent thermal management. These systems monitor real-time temperature data and adjust cooling or heating dynamically based on operating conditions. Predictive algorithms and connectivity features enhance efficiency, reduce energy consumption, and improve reliability, supporting the broader trend toward connected and autonomous vehicle technologies.

Automotive Heat Exchanger Market Analysis

Learn more about the key segments shaping this market

Download Free PDF

Based on vehicle, the market is divided into passenger cars, commercial vehicles, and off highway vehicle. The passenger cars segment dominated the automotive heat exchanger market, accounting for around 65.5% in 2025 and is expected to grow at a CAGR of more than 8.7% through 2035.

Based on sales channel, the market is categorized into OEM, and aftermarket. The OEM segment dominates the market accounting for around 72.2% share in 2025, and the segment is expected to grow at a CAGR of over 8.3% from 2026-2035.

Based on material, the automotive heat exchanger market is divided into aluminum, copper, and others. The Aluminum segment held the major market share in 2025.

Based on product, the automotive heat exchanger market is divided into radiators, intercoolers, oil coolers, exhaust gas recirculation (EGR), and others. The radiators segment dominated the market.

China dominated the automotive heat exchanger market in Asia Pacific with around 64.2% share and generated USD 11 billion in revenue in 2025.

The automotive heat exchanger market in Germany is expected to experience significant and promising growth from 2026 to 2035.

The automotive heat exchanger market in US is expected to experience significant and promising growth from 2026-2035.

The automotive heat exchanger market in Brazil is expected to experience significant and promising growth from 2026 to 2035.

The automotive heat exchanger market in UAE is expected to experience significant and promising growth from 2026-2035.

Automotive Heat Exchanger Market Share

Automotive Heat Exchanger Market Companies

Major players operating in the automotive heat exchanger industry are:

BorgWarner

Dana

13.8% market share

Collective Market Share in 2025 is 55.6%

Automotive Heat exchanger Industry News

The automotive heat exchanger market research report includes in-depth coverage of the industry with estimates & forecasts in terms of revenue ($Bn), and shipment (Units) from 2022 to 2035, for the following segments:

Click here to Buy Section of this Report

Market, By Vehicle

Market, By Product

Market, By Material

Market, By Design

Market, By Sales Channel

Market, By Propulsion

The above information is provided for the following regions and countries: